After a volatile June, July brought calmer oil markets, with West Texas Intermediate (WTI) prices holding between $60 and $70 per barrel—my expected range for August as well. In early July, the eight voluntary OPEC+ members increased their production limits by roughly 550,000 barrels per day. I expect these members to announce another 550,000 barrels per day increase in early August.

I am curious how oil markets will react after Labor Day, when the US driving season and Middle East air conditioning demand taper off. Recent production increases by the voluntary OPEC+ nations were partially absorbed by their heightened air conditioning needs. Eric Nuttall and Paul Sankey, in recent YouTube videos, express caution about oil’s fourth-quarter outlook.

On July 21, The Wall Street Journal published “How China Curbed Its Oil Addiction—and Blunted a U.S. Pressure Point.”

BEIJING—China’s thirst for oil drove global demand for decades. Now a government campaign to curb that addiction is nearing a milestone, with national consumption expected to peak by 2027, then begin to fall.

Chinese officials have long worried that the U.S. and its allies could hamstring the nation’s economy by choking off its supply of foreign oil. So China has poured hundreds of billions of dollars into weaning itself off the imported stuff by reviving domestic production and swiftly building the world’s leading electric-vehicle industry.

…

Across China, fleets of gas-guzzling Volkswagen and Hyundai taxicabs are being replaced by electric models designed and produced locally. Last year, nearly half of passenger vehicles sold in the country were either all-electrics or plug-in hybrids, compared with 6% in 2020.

I am skeptical of China’s oil demand peaking by 2027. Its weakened economy over recent years has curbed consumption, with renewables also displacing oil. As China’s economy recovers, I expect rising energy needs to drive increased oil use. China’s trajectory is key to oil’s long-term outlook, but traders do not expect a major impact this year.

Disclosure: Short strangle (short calls and short puts) on WTI futures.

June was an especially challenging and turbulent month with the twelve-day war in Iran. Because of the war, West Texas Intermediate (WTI) oil prices for June exceeded the high end of my target range of $67.50. Now that the war is behind us, I expect WTI to range between $60 to $70 per barrel for July.

I will share some of the news items during the past month that have influenced my thinking. On May 31, the Financial Times published “Opec+ to boost oil output for third consecutive month” (subscription required).

Opec+ announced another large increase in oil output for July in the latest sign that the cartel was intent on unwinding the first tranche of its long-standing production cuts as quickly as possible.

Eight members of the oil-producing group, including Saudi Arabia and Russia, said on Saturday that they would increase headline production in July by a combined 411,000 b/d.

The decision to fast-track the return of idled capacity for the third consecutive month means the group could add as much as 1.4mn b/d to the global market between April and the end of July.

Like many others, I expect another headline in early July saying that production will be increased by another 411 kbd for August.

Another article by the Financial Times on June 2 “Saudi Aramco raises $5bn in bond sale as it grapples with lower oil prices” (subscription required) hints that lower prices might be here to stay for a while.

Saudi Aramco, the world’s largest oil company, said on Monday it had raised $5bn in a bond sale as it positions for a downturn in oil prices and prepares for further borrowing.

Aramco said demand for the three sets of bonds it issued in London had been “strong”, with coupons ranging from 4.75 per cent to 6.375 per cent.

The issuance was one of the largest in London so far this year, after the Public Investment Fund, the Saudi sovereign wealth fund, tapped the debt market for $4bn in January, and UK building society Nationwide sold €3.25bn and £1bn of bonds during the first quarter.

One of the many people that I admire and follow on X is Gary Ross.

Oil bull for now! Stocks still low, about to close over 50 day, runs seasonally incr, S&P looks good, weak $, positioning is short, geopolitical risks to supply are sign (sanctions incr Iran/Rus & Libya–TACO may surprise-+ bull weather events. See 70$ before return 5 handle!!

On June 4, Bloomberg published a short article “Saudi Arabia Wants More Super-Size OPEC+ Hikes” (subscription required).

Saudi Arabia wants OPEC+ to continue with accelerated oil supply hikes in the coming months as it puts greater importance on regaining lost market share, according to people familiar with the matter.

The kingdom, which holds an increasingly dominant position within OPEC+, wants the group to add at least 411,000 barrels a day in August and potentially September, the people said, asking not to be named because the information was private. Riyadh is keen to unwind its cuts as quickly as possible to take advantage of peak demand during the northern hemisphere summer, one person said.

Although I agree with the 411 kbd increase, I am less confident of the rationale.

On June 10, the Financial Times published “US oil output set for first annual drop since pandemic” (subscription required).

US oil production will fall next year for the first time since the Covid-19 pandemic, according to a government forecast that will cast new doubt on Donald Trump’s “energy dominance” agenda.

The Energy Information Administration, a division of the energy department, on Tuesday said US oil production would drop from a record high of 13.5mn barrels a day now to about 13.3mn barrels by the end of next year, as slumping oil prices rattle the sector.

“With fewer active drilling rigs, we forecast US operators will drill and complete fewer wells through 2026,” the EIA said in a monthly report published on Tuesday. Active rigs had “decreased by much more” than expected in a previous report, it said.

This development adds to the bullish sentiment.

Another June 10 article, this one from the CBC “OPEC boss slams net-zero targets, promotes big future for oil in Calgary speech” (free access) suggests that demand for oil and gas has a long horizon.

“Simply put, ladies and gentlemen, there is no peak in oil demand on the horizon. The fact that oil demand keeps rising, hitting new records year on year, is a clear example of what I’m saying,” he said in his speech.

Primary energy demand is forecast to rise by 24 per cent between now and 2050, he said, surpassing 120 million barrels of oil a day. Currently, oil demand is around 103 million barrels per day.

“Meeting this ever-rising demand will only be possible with adequate and timely and necessary investments in the oil industry,” he said, pointing to the need for $17.4 trillion US in investment over the next 25 years.

In contrast to the CBC article, the Financial Times published “Big Oil faces up to its sunset era” (free access) where the title suggests that the industry is dying.

Oil majors are no strangers to boom-and-bust cycles. But now the challenge may be structural. The rapid adoption of electric vehicles, especially in China, has surprised the industry. Many oil majors now concede that their production will probably peak within the next decade.

“There’s no doubt that in the grand scheme of things, this is a sunset industry,” says Paul Gooden, head of natural resources at asset manager Ninety One. “We can debate how far the sunset is away, but companies need to recognise that — and increasingly they are recognising that.”

László Varró, Shell’s head of scenario planning, echoes the sentiment. “There is very little doubt that peak oil demand is coming,” he says.

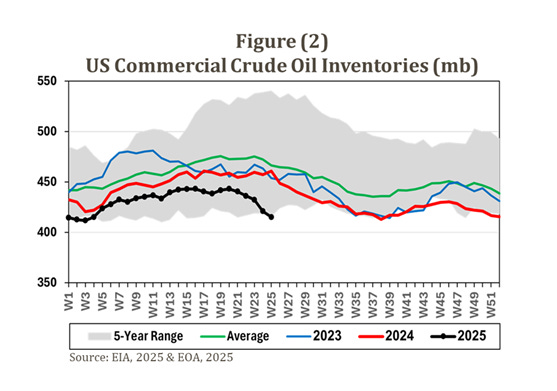

The US Commercial Crude Oil Inventories (MB) chart comes from Dr. Anas Alhajji’s subscription-based Daily Energy Report.

US Commercial Crude Oil Inventories

Because oil inventories have broken below their five-year range, I am moderately supportive of oil prices. The macroenvironment still looks challenging; however, oil inventories are low and trending lower.

I deliberately avoided discussing the war in Iran. Numerous media organizations covered it extensively, and I am hoping that because the war is behind us, we are back to normal oil markets.

Switching topics, I want return to an earlier period in June when there were a lot of pessimistic price outlooks. Some investment banks were calling for Brent prices to remain in the low $60s for the remainder of the year.

I am going to mention two individuals that have been or are bearish, comparatively speaking, on the oil price outlook. Even though their views are different than mine, I have great respect for both individuals. If I mention someone in my articles who takes an opposing view to mine, it is usually because I respect their viewpoints and want to allow others to consider those viewpoints. If I do not have respect for someone’s outlook, I simply do not mention them, regardless of whether I agree with them.

As I mentioned last week, it is rare that I have a more bullish outlook than Eric Nuttall. Here is his latest YouTube which was published on June 5 before the war in Iran:

On June 2, Paul Sankey from Sankey Research provided some bearish comments on CNBC. You can follow through his X post to CNBC to watch the video:

Global oil market at historic inflection point as supply, demand falls, says Paul Sankey @CNBChttps://t.co/BqDzibr8IH

And then on June 11, Sankey provides more context to his CNBC comments in a YouTube video:

I found his YouTube presentation quite interesting and informative.

Overall, I am moderately supportive of slightly higher prices for July. As mentioned at the outset, I expect WTI to range between $60 to $70 per barrel for July. Although I am moderately supportive of oil prices for July, I am less sanguine about oil prices in the fourth quarter. As we get close to the fourth quarter, I may revise my outlook.

Disclosure: Short strangle (short calls and short puts) on WTI futures.

After another turbulent, challenging month for West Texas Intermediate (WTI), my expectations for WTI prices in June are reduced by $2.50 per barrel. I expect WTI to range between $57.50 to $67.50 per barrel.

Tariff and geopolitical issues as well as the “voluntary eight” of the OPEC+ reducing their production cutbacks continued to stress oil prices in April. These concerns will not be resolved in May. The voluntary eight OPEC+ countries that have reduced their production cutbacks are Saudi Arabia, Russia, Iraq, UAE, Kuwait, Kazakhstan, Algeria, and Oman. There remain concerns that Iraq and Kazakhstan are producing more than their quotas. As a consequence, in early June, many expect the voluntary eight members of OPEC+ to raise the production ceiling by another 411 thousand barrels per day. The reality is that because Middle East countries burn more oil to meet their cooling needs during the hot summer months, much of the increased production is never exported. In other words, OPEC+ exports during the hot summer months are largely unaffected by these production increases.

I do not have much confidence in my outlook because of the uncertainty surrounding the previously mentioned challenges. In this article, I will provide some of the sources that I relied upon to reach my outlook.

The Financial Times May 11 article “Saudi Aramco cuts its dividend by $10bn” (subscription required) gave me pause because oil companies are loathe to cut their dividends. When dividends are cut, it suggests an anticipation that current or worse conditions may exist for a while. Shareholders of companies rely upon dividends remaining the same or increasing and may flee from companies that reduce their dividends, thereby driving down share prices.

The world’s largest oil company’s net income dropped 5 per cent from a year earlier to $26bn. Its average realised oil price was $76.30 a barrel, compared with $83 a barrel in the same quarter last year.

While the performance was better than that of some of its peers, including BP and Shell, whose first-quarter profits halved and fell by 28 per cent respectively, Aramco cut its total dividend to $21.4bn from $31bn in the final quarter of last year.

There were two important articles regarding peak shale. The Wall Street Journal May 17 article “U.S. Drillers Say Peak Shale Has Arrived” (subscription required) suggests that shale production is challenged at these prices.

Drillers that made the U.S. the world’s top oil producer say they are hitting the brakes to weather a period of low crude prices and that the gusher has likely peaked. Some of the largest producers, including Diamondback Energy, recently told investors that they would be spending less this year and plan to drop rigs.

The U.S. is on track to see crude oil production modestly increase in 2025—in part because of growth in fields offshore—before declining next year by 1% to 13.33 million barrels a day, according to S&P Global Commodity Insights. That would mark the first year-on-year decrease in roughly a decade, outside the Covid-19 pandemic.

“We believe we are at a tipping point for U.S. oil production at current commodity prices,” Travis Stice, chief executive of Permian driller Diamondback, said in a letter to shareholders last week.

Next, the Financial Times May 25 article “Oil chiefs warn of end to US shale boom” (subscription required) also suggests shale production is challenged.

“We’re on high alert at this point,” Clay Gaspar, chief executive officer at Devon Energy in Oklahoma City, told investors this month. “Everything is on the table as we move into a more distressed environment.”

Oil output will fall by 1.1 per cent next year to 13.3mn barrels a day, according to S&P Global Commodity Insights, as prolific shale drillers that made the US the world’s biggest producer idle rigs in the face of prices driven lower by fears of oversupply and Trump’s trade war.

That would mark the first annual decline in a decade, excluding the 2020 pandemic when collapsing demand sent oil prices below zero and triggered widespread bankruptcies across states such as Texas and North Dakota.

If shale production plateaus or recedes slightly, then that is bullish for oil prices because there is less oil on the market.

With all turbulence, however, there are some economic concerns.

Serious Credit Card Delinquencies (unpaid balances for at least 90 days) just hit their highest level in 14 years 🚨🚨🚨 pic.twitter.com/3YewHU0H0E

Rising delinquent credit card and car payments show that consumers are struggling. Once tariffs hit, consumers are likely to be even more stressed.

The Bloomberg May 22 article “OPEC+ Discusses Another Super-Sized Output Hike for July” (subscription required) suggests that another large increase in the production ceiling may be decided in early June.

OPEC+ members are discussing making a third consecutive oil production surge in July, to be decided at the group’s meeting in just over a week, delegates said.

An output hike of 411,000 barrels a day for July — triple the amount initially planned — is among options under discussion, although no final agreement has yet been reached, said the delegates, asking not to be named because the information is private. A final decision is due to be taken at a gathering on June 1.

The cartel has helped sink crude prices since announcing 411,000-barrel hikes for May and June — equivalent to about 1% of current OPEC+ output — in a historic break with years of defending oil markets. Oil made a fresh plunge on Thursday, dropping 0.9% to $64.31 a barrel as of 9:13 a.m. in London.

This is one of the rare times that I am more bullish on oil prices than is Eric Nuttall. Below is a thirteen-minute YouTube video by Nuttall.

Another fund manager that I follow is Josh Young. Below are two posts on X where he expresses his bullishness:

I am not as bullish as Josh because the economic backdrop is likely to contain any exuberance.

I follow people whose viewpoints are varied and keep an open mind because the oil price environment can be and often is extremely volatile.

Another person I like to follow on X is Dr. Anas Alhajji because he has an in-depth understanding of the oil market and is able to follow and correspond with folks in the Middle East. The following X post references a 90-minute YouTube video. If you want a deep dive into the crude markets, the video is worth watching.

TFTC 621 w/ @anasalhajji: "BRICS is a paper tiger… The dollar is here to stay and the petrodollar is here to stay."

We discuss: ⚡️ Trump in the Middle East ⚡️Crude markets, trade war and US debt ⚡️Trump's energy stance ⚡️AI and bitcoin pic.twitter.com/iILhBfHPAe

The outlook is far from certain. There are well-respected fund managers who are either bearish or bullish. My own view tends to expect more of the same. While OPEC+ is unlikely to flood the oil market, Saudi Aramco’s dividend cut warrants attention. The global economy is constantly reacting to the latest developments by the US administration. And American consumers are showing signs of being stretched. All these factors lead me to believe that WTI prices are likely to remain with the range of $57.50 to $67.50 for the next month.

After a turbulent April, my expectations for West Texas Intermediate (WTI) oil prices in May are $5 less per barrel April. I expect WTI to range between $60 to $70 per barrel.

As we are all aware, April was a challenging month. Most investors expected OPEC+ to hold steady on production increases. Instead, it brought three months of production increases forward. And the US administration surprised investors with a harsher than expected set of tariff demands, especially against China. Many in the investment and business communities have commented that, although the tariffs themselves are detrimental to the business climate, the volatility and uncertainty is even worse. Because the business pages of major online newspapers have been filled with analysis and commentary about the tariffs and what they may mean for the US and global economies, I do not intend to belabor the issue here.

That said, Wall Street banks have cut their S&P 500 year-end targets. On April 18, when the S&P finished at 5,283, the Financial Times published “Wall Street slashes stock market forecasts amid Trump tariff fears” (subscription required) with the following chart:

A graph presented by the Financial Times showing prior and current S&P 500 target values.

These lower targets reflect anticipated diminished economic activity and profits. With less economic activity and potentially more oil output from OPEC+, oil prices are also expected to be lower.

In early May, I expect OPEC+ to once again increase production. In the strictest sense, it is not OPEC+ but rather the “voluntary eight” countries that had earlier reduced their production to now increase their production from current levels.

Some are attributing this increased production as punishment to those countries who have not honored their commitments to reduce production. I prefer Dr. Anas Alhajji’s explanation that the increased production level more easily allows the overproducers to meet their targets. If punishment or retribution were the goal, OPEC+ would take more drastic actions, as it has done in the past.

In the past few monthly updates, I have provided links to Eric Nuttall’s videos. He is more cautious on oil prices going into OPEC+’s decision. Here is his five-minute YouTube video:

Oil is always volatile. And it is especially volatile with so much uncertainty surrounding tariffs and other geopolitical issues.

My expectation for April West Texas Intermediate (WTI) oil prices are slightly less than they were for January and February. I reduced the range endpoints by $2.50 per barrel to range between $65 to $75 per barrel. February WTI prices pierced my lower end of $67.50 during the markets squall in mid-March.

Last month, I mentioned lack of consumer confidence. Consumer confidence is likely to continue to be weak as the US administration announces new tariffs on April 2 and countries respond. Uncertainty around the globe is likely to increase, and consumers are likely to be cautious until they understand how the new environment affects them directly.

During the past two months, oil stocks have been surprisingly strong even though oil prices have been moderate. Barron’s Magazine noted the same observation in a recent article from March 27 “An Oil Stock Riding the ‘Dune Express’ to Success in an Uncertain Energy Rally” (subscription required).

The energy sector shouldn’t be doing this well. It’s the best-performing sector in the S&P 500 this year, despite crude prices sliding a bit. The return of President Trump to the White House has boosted hopes that the federal government will continue to push for increased U.S. oil production and less on renewable sources of power, something that could lead to a glut of unused oil—and lower prices still. Perhaps the markets are sniffing out something the headlines aren’t—or maybe the energy sector is just getting ahead of itself.

My guess—and it is only a guess—is that investors have become more cautious on the high-flying magnificent seven stocks and have allocated some of their capital to solid stocks with higher paying dividends and with reasonable price-to-earnings multiples. Unfortunately, there is no way to know with any confidence.

Once again, I present Eric Nuttall’s commentary. I agree with most of what he says with the exception that I am not quite as bullish as he is on oil prices, at least not in the next month.

Sanctions against Iran have largely been ineffective in the past, and I expect that they will be ineffective going forward. As mentioned, tariffs are likely to introduce more caution and uncertainty around the globe. For the next month, I expect oil prices to remain soft.

The lower end of my price target at $65 is if the markets come under significant duress. And $75 is if the new tariffs are largely irrelevant, and everyone is happy again.

In his comments, Nuttall mentioned the Dallas Fed. It is interesting to note that the average expectation for oil prices six months from now is $68 and one year from now is $70.

Another page worth reviewing is the Comments tab. Here are three comments from that page:

The administration’s tariffs immediately increased the cost of our casing and tubing by 25 percent even though inventory costs our pipe brokers less. U.S. tubular manufacturers immediately raised their prices to reflect the anticipated tariffs on steel. The threat of $50 oil prices by the administration has caused our firm to reduce its 2025 and 2026 capital expenditures. “Drill, baby, drill” does not work with $50 per barrel oil. Rigs will get dropped, employment in the oil industry will decrease, and U.S. oil production will decline as it did during COVID-19.

I have never felt more uncertainty about our business in my entire 40-plus-year career.

Uncertainty around everything has sharply risen during the past quarter. Planning for new development is extremely difficult right now due to the uncertainty around steel-based products. Oil prices feel incredibly unstable, and it’s hard to gauge whether prices will be in the $50s per barrel or $70s per barrel. Combined, our ability to plan operations for any meaningful amount of time in the future has been severely diminished.

Like I said, uncertainty is on the rise until there is more clarity regarding tariffs.

In summary, my expectation for WTI oil prices for April is $65 to $75 per barrel.

Recent Comments